2026 Private Markets Outlook: Trends & 2025 Recap

Private markets in 2026 reflect greater discipline, wider dispersion, and an expanding role for private wealth.

.jpg)

TL;DR

- 2025 marked a fragile soft landing: Inflation easing, rates edging lower, more deals, better exits, record secondaries and private credit going mainstream.

- 2026 shaped by structural forces: AI as the main growth engine, energy and infrastructure reinvention, tougher trade politics, and a fading divide between public and private markets.

- Dispersion will grow by asset class: Private equity shifts back into deployment, private credit matures but sees more stress, infrastructure for “beds, sheds, bytes” sees further success, and IPO pipelines reopen.

- HNWIs and family offices move centre stage: Stepping into funding gaps, using co-investments and SPVs, and competing with institutions in real estate, secondaries and late-stage tech.

- Wealt helps make this accessible: Lowering minimums and fees, improving transparency and liquidity, and giving private investors curated access to deals in tech, AI, defence and energy.

As we move from 2025 into 2026, private markets are transitioning from a stabilisation phase to a more disciplined, fundamentals-driven phase. The past year brought cooler inflation, clearer interest rate expectations and a gradual normalisation of deal activity, giving investors better forward visibility after several volatile cycles. The year ahead is likely to be defined less by macro shocks and more by how capital is allocated across structural themes such as AI, infrastructure, secondaries, and the growing role of private credit. This matters in particular for high-net-worth investors and family offices, who are no longer peripheral participants in private markets but have the tools to be deliberate about how they use private assets to build resilient, long-term portfolios.

What shaped markets in 2025?

As we turned the page to 2025, the story shifted from crisis management to cautious rebuilding. The shock of post-pandemic inflation and rate hikes faded into the background; growth slowed but held together, inflation came down in most major economies, and central banks carefully nudged policy toward rate cuts. Politics was a significant part of the year, with a new US administration doubling down on tariffs and wars ongoing in Europe and the Middle East. None of this, however, was enough to derail the narrative that the world has stepped back from the brink of a brutal recession. In markets, equity indices marched higher, AI-heavy tech led the charge, and volatility quietly trended lower as investors decided they could live with the higher rates.

In private markets, 2025 felt like the first real year of forward motion. Asset valuations stabilised, bid-ask spreads narrowed, and dealmakers discovered an appetite for carve-outs, public-to-privates and structured solutions. Exits improved but did not fully normalise, so record secondary volumes effectively became a parallel exit lane, giving LPs a way to recycle capital and GPs more time with their best assets. Private credit cemented its role as a mainstream financing channel rather than a niche. Real estate reset, with capital flowing out of obsolete offices and into logistics, living and data infrastructure. And over all of it hung the AI boom and a renewed push into climate and energy security.

Macro environment

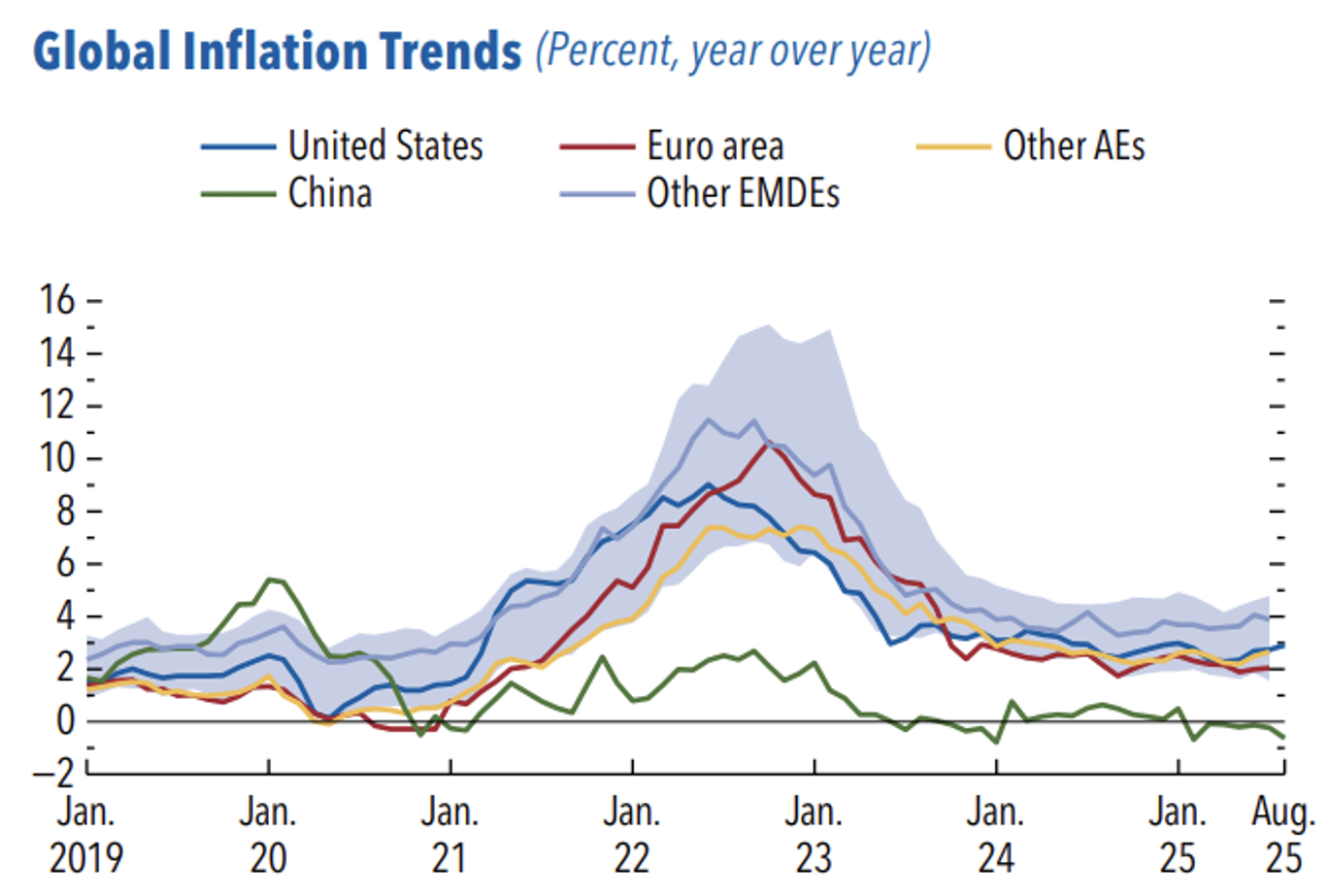

Many have described the global macro picture in 2025 as mirroring a fragile soft landing. After the post-pandemic spike, headline inflation continued to decline, with the IMF projecting global inflation at about 4.2% in 2025 and 3.6% in 2026, much closer to normal in many economies. This allowed the Fed, ECB and Bank of England to start a cautious rate-cutting cycle. Forecasts from the IMF project global growth slightly above 3% this year, weaker than pre-pandemic trends but better than feared, with ongoing risks from trade tensions, conflict, and supply chain fragmentation still on the radar.

Public markets responded positively to this mix of lower inflation, gently easing rates and resilient earnings. Major developed equity indices delivered solid double-digit gains over the year, led by the US and large European markets, and volatility trended down from the spikes of 2022 and 2023. That improvement in sentiment, combined with more stable financing conditions, helped global M&A move decisively off the bottom, with total deal values estimated to be up 36% to about 4.8 trillion dollars, up from 2024.

With Donald Trump re-entering the Oval Office, the beginning of his second term was marked by a clear shift toward tariff-driven policy and strategic trade, even as growth and trade volumes continued to rise. The US rolled out “reciprocal” tariffs on major partners, the European Union imposed anti-subsidy duties of roughly 7-35% on Chinese electric vehicles, and countries such as Mexico introduced steep tariffs on a wide range of Chinese and Asian imports. As trade is channelled within geopolitical blocs, this marks the beginning of “geoeconomic fragmentation”, a turning point away from the globalisation of the last couple of decades.

.png)

Exits, liquidity & secondaries

While exit and liquidity conditions in private equity improved in 2025, the industry still struggled to manage its asset backlog. After two weak years, PE-backed exit values rose again, helped by a modest reopening of the IPO window and by more strategic buyers returning to the market, particularly in sectors such as healthcare, industrials, and infrastructure. Yet holding periods remain extended, and many sponsors are still struggling to find sufficient buyers for the large volume of assets approaching fund maturity. As a result, DPI metrics across many portfolios remain below long-term averages.

With traditional exit routes not enough to clear portfolios, secondaries have become a primary source of liquidity for LPs and a strategic tool for ageing GP portfolios. Global secondary transaction volume reached $103B in H1 2025, up 51% year on year, with LP-led deals totalling $56B and accounting for 54% of activity, and GP-led volume at $47B, up 68% versus H1 2024. In practice, this meant LPs used portfolio sales to recycle capital and reshape allocations, while GPs relied on continuation vehicles to retain high-conviction assets and provide liquidity to investors without forcing outright exits in a still uneven market.

.png)

Fundraising

Fundraising in 2025 stayed challenging even as markets improved. Global private equity vehicles raised roughly $580B in the twelve months to September, slightly below the prior year and far from the 2021 peak. With a couple slow years for exits, LPs were still cash constrained and highly selective, largely seen as the weak spot within a otherwise improving PE landscape.

Within that smaller pool of capital, concentration intensified drastically. In the US, nearly 46% of all PE cash raised in 2025 went to the ten largest funds, up from 35% in 2024, while first time funds closed at record low amounts. At the same time, LPs moved away from blind pool commitments and took part in more targeted exposure, with statistics showing around 80-90% of institutional investors now planning to allocate up to 20% of their PE capital to co-investments.

.png)

Deployment

By contrast, deployment has been more constructive. With valuation expectations finally resetting, 2025 saw a solid recovery in deal activity across buyouts, private credit, and infrastructure, even if volumes remained below the 2021 peak. Early 2025 deal value in global buyouts was materially higher, before moderating mid-year as sponsors navigated the macro environment. Dry powder across private equity started the year around $2.25T; however, it has been consistently trending down as managers have leaned into public-to-private opportunities, complex carve-outs, and secondary solutions.

Deal flow skewed toward larger and more complex transactions, as large buyouts drove much of the recovery, especially in North America and Europe. Public to private takeovers remained a key theme in Europe and the UK, where valuation gaps on listed markets created opportunities for take privates, while across regions, sponsors increasingly combined equity with private credit solutions to navigate a relatively fragile lending environment. Overall, the year was about the selective deployment of dry powder into the deals that fit the long-term macro themes of the coming years.

Private credit momentum

2025 has seen private credit cementing itself as a core asset class within private markets rather than a niche, last resort lender. On the fundraising side, private credit funds raised about $146.9B in H1 2025, comfortably ahead of both 2023 and 2024. The geography of that capital is shifting too, with Europe-focused strategies rising nearly threefold from 2024 as allocators rebalanced away from a prior overweight in US direct lending.

For borrowers, higher base rates and tighter bank regulation kept demand strong for flexible, private solutions. For investors, private credit offered an appealing combination of income, floating-rate protection, and lower mark-to-market volatility than public credit. Only 38% of private credit fundraising dollars in H1 2025 went into traditional direct-lending funds, down from 57% the year before, with more capital flowing to opportunistic, special-situations, and fund-of-funds vehicles.

.png)

Cryptocurrency

For crypto, 2025 was a consolidation year, with Bitcoin's full-year return of around -5% following the significant gains of 2023 and 2024. Despite this relatively flat performance, institutional adoption quietly accelerated, with around 55% of global hedge funds holding some form of crypto exposure, even if most still keep allocations below 2% of AUM.

The broader digital asset ecosystem grew faster than headline coin prices. Stablecoin supply climbed to around $300B by September, with usage metrics showing that stablecoins now account for about 30% of all crypto transaction volume and more than $1.25T in transfers in a single month. Large incumbents such as JPMorgan also launched tokenised money market funds on public blockchains, and global regulators tightened and clarified rules through frameworks, pushing digital assets further into the mainstream while putting more emphasis on transparency and protection.

.png)

Real estate

Global real estate in 2025 shifted toward a slow, uneven recovery, with global office leasing at its highest level since 2019 and vacancy starting to fall in prime central locations as new construction hits decade lows. Older, energy-inefficient offices and weaker retail stock continue to reprice, while top-tier offices, logistics, living, and niche operational assets attract most of the capital. On the residential side, tight housing supply kept rental growth elevated and reinforced investor focus on build-to-rent, student housing and nursing care.

The repricing in commercial property created an opportunity for private investors, especially high-net-worth individuals and family offices, to re-enter the market. At the same time, large institutions remained cautious and selective. As institutions cut back real estate allocations after the stress of 2023–24, this funding gap was filled mainly by private capital, helping to stabilise pricing for prime assets and keep deals moving in sectors with stronger fundamentals.

AI bubble

Throughout the year, the AI trade dominated markets, with prices and expectations racing ahead of fundamentals. By late 2025, the Magnificent Seven accounted for roughly 30% of the S&P 500’s market cap, and some AI leaders were trading at forward price-to-earnings multiples in the 50–70 range, levels similar to those during the 1990s tech boom. The sector has been one of the most significant macro drivers, with AI capex adding approximately 1.1 percentage points to US GDP growth in H1 2025.

This backdrop has sparked ongoing discussion of an AI bubble, in which the market may be moving much faster than the underlying technology and financial performance of firms in the sector. Parallels have been drawn to the dot-com crash, with events such as Oracle's 15% one-day drop following the release of disappointing AI-related results, fueling fears about overvalued shares. While sentiment is mixed on the merits of current AI valuations, what is less contested is that AI will fundamentally reshape how we live and work, even if the economic payoff remains uncertain.

.png)

Infrastructure

Infrastructure in 2025 was one of the clearest long-term winners in private markets. On the clean-energy side, capital continued to flow into solar, batteries, and, increasingly, grid upgrades, interconnectors, and storage. In the digital infrastructure sector, hyperscale data centres, fibre, and towers all benefited from surging AI and cloud demand, with developers racing to secure scarce grid capacity and power in key hubs. At the same time, investors increasingly framed infrastructure through a broader security lens, with growing interest in defence and dual-use assets such as secure communications, cyber and space systems, alongside traditional energy transition projects.

Offshore wind, by contrast, had a challenging year. After a long period of rapid expansion, the sector hit a rough patch in 2025 as rising costs, supply chain bottlenecks and more demanding auction designs squeezed project economics. Several European sites and offtake auctions attracted no bidders, including high-profile tenders in Germany and Denmark, forcing governments and developers back to the drawing board on contract structures and support schemes.

.png)

The forces reshaping markets in 2026

Looking ahead to 2026, private markets are entering a more mature yet still opportunity-rich phase, driven less by emergency macroeconomic conditions and more by profound structural shifts in technology, energy, and geopolitics. The traditional boundaries between public and private markets are softening, secondary markets and private credit are becoming core liquidity and financing channels, and regulators are steadily raising the bar on transparency and access. At the same time, AI and digital infrastructure, the energy and security transition, and changing demographics are reshaping where capital is needed and how quickly it must move. Against that backdrop, 2026 will be about learning to operate in a more fragmented, politically charged, and occasionally volatile world, and seeing which players in each private-market asset class can navigate these challenges.

The forces reshaping markets in 2026 are likely to be:

- Public & Private markets - In 2026, the line between public and private markets is set to blur further. In the UK, new PISCES platforms will allow private companies to run periodic, exchange-style trading windows for their shares without a full IPO, providing quasi-public liquidity while maintaining tight control over trading and disclosures. In the US, the SEC’s Investor Advisory Committee has endorsed the view that retail investors should access private assets primarily through registered funds that mix public and private holdings. As a result, portfolios on retail platforms will increasingly include both listed stocks and unlisted deals in a single wrapper.

- Technology as the primary growth driver - In 2026, AI is set to remain the primary driver of both capital spending and earnings growth. Institutions view AI as a genuine general-purpose technology that can boost productivity and growth, but warn that the payoff is uncertain and front-loaded for a small group of companies and sectors. That mix of massive real-world investment, concentrated stock market leadership, and still-unproven long-term economics is exactly why 2026 is likely to be defined by AI.

- Energy and infrastructure reinvention - The energy transition is likely to continue to see large amounts of capital flowing into grids, storage, renewables, and other critical assets, with the narrative shifting away from pure decarbonisation toward energy security and resilience. At the same time, rising defence budgets and shifting ESG attitudes are pulling defence, cyber, space and other dual-use technologies into the mainstream.

- Geographic realignment - In 2026, the political backdrop is likely to be defined by a more fractured but still interconnected global economy. A second Trump administration in the US is expected to maintain elevated tariffs and reciprocal trade measures, while China, Europe, and key emerging markets respond with targeted industrial policies and tougher trade strategies. Trade is likely to become more regionalised, with supply chains and commerce increasingly concentrated within politically aligned blocs and neighbouring economies rather than flowing freely at a fully global scale.

- Monetary and fiscal policy - After the post-pandemic inflation shock, major central banks will continue shifting from aggressive tightening to cautious easing, cutting rates slowly to avoid reigniting price pressures. At the same time, governments have emerged from years of emergency spending with higher structural deficits and rising debt-service costs, yet face intense pressure to maintain high levels of funding. That combination will mean public balance sheets remain under closer scrutiny, and fiscal choices on taxes, subsidies and tariffs become a central driver of winners and losers.

Private credit

Private credit is likely to remain one of the most dynamic parts of private markets in 2026, but it will shift from an emerging niche to a mature ecosystem. After several years of rapid growth and strong fundraising, the market is expected to continue expanding, supported by falling base rates that gradually ease pressure on highly leveraged borrowers. Lenders are also moving beyond classic unitranche loans into more creative solutions. As the boundaries between public and private credit continue to blur, large managers are likely to develop a suite of products spanning the entire credit spectrum, from investment-grade to opportunistic.

On the other hand, 2026 also appears to be a year of more visible credit stress. After a wave of high-profile restructurings, default rates in some segments are expected to peak. Some rating agencies still describe the ~$3T market as fragile, with weaker borrowers facing margin compression and thinner interest coverage. Overall, this means 2026 will likely be less about a blanket view on all private credit and more about understanding the nuances that drive some firms to succeed while others do not.

Private equity

2026 could be the year private equity finally emerges from its slump and starts to rebuild some of the reputation it lost. Years of muted deal activity and extended holding periods have left the industry with roughly $2T in dry powder. As rates edge lower, the secondaries market deepens, and the IPO window gradually reopens, the stage is set for a healthier deal environment with more realistic valuation expectations. Alongside classic buyouts, we are also likely to see more public-to-private takeovers of listed companies and corporate carve-outs of non-core business units.

At the same time, any recovery will look very different from the pre-COVID boom. A higher cost of capital, more intrusive politics and tighter regulation will make value creation more hands-on and operationally intensive. Competition from private credit and secondaries will influence how deals are structured and how liquidity is managed throughout a fund's life. The winners in 2026 are likely to be managers who can deploy at scale while bringing real-sector insight across tech, healthcare, and tangible assets, and who can provide LPs with credible, repeatable paths to liquidity rather than relying on headline IRRs alone.

.png)

Secondaries

In the secondaries market, GP-led deals are expected to capture a growing share of volume as sponsors use them to manage holding periods, recycle capital, and align with new investors. Platforms serving private wealth, like Wealt, are also building their own secondary marketplaces, enabling high-net-worth investors to trade stakes in private funds more easily and adding a new layer of liquidity on top of traditional institutional deals.

Secondaries are set to remain a core liquidity engine in 2026 after a record-breaking 2025. With LPs needing liquidity and portfolio rebalancing after slow exits, and GPs facing ageing funds with substantial assets but limited traditional exit options, secondary deal flow will remain elevated. In a similar story to private credit, secondaries will evolve from a last resort to a standard tool used in portfolio management, and with such a significant backlog, will likely see its total AUM growth outpace that of traditional private equity.

Infrastructure

Infrastructure is positioned for another strong year in 2026, at the crossroads of three major forces: AI and data, the energy transition, and supply security. As electricity demand rises, ageing networks are being replaced, and economies electrify transport, industry, and heating, the roadmap for future capex needs remains crowded. AI will continue to radically accelerate demand for data centres and the power required to run them. Multiple 2026 outlooks indicate that US data centre power demand alone will reach more than 50 gigawatts by 2028 and potentially over 100 gigawatts by 2035.

After years of trading at a premium to global equities, listed infrastructure now trades at one of its widest relative valuation discounts, even though long term investment needs in energy, grids and digital networks are accelerating. Much of this discount can be attributed to uncertainty around the path of interest rates rather than to deteriorating fundamentals, which suggests a more attractive entry point for patient capital. In 2026, the focus is therefore less on whether there is demand for infrastructure and more on which managers can secure scarce power and grid connections, navigate policy and permitting risk, and build platforms that can keep pace with the scale and speed required in the modern climate.

.png)

Real estate

Lower but still elevated interest rates and easing inflation should support a gradual rebound in transaction volumes and capital values in 2026, especially in sectors with clear structural tailwinds such as logistics, living, and high-quality offices. Investors are expected to return to asset-level fundamentals, with building quality, energy efficiency and broader ESG performance becoming key drivers of pricing, financing and exit liquidity.

At the same time, there will be further divergence for certain assets, specifically energy inefficient offices and assets in weaker locations. Such buildings are likely to continue to be repriced and eventually repurposed into residential or mixed-use schemes. This marks a very different story from the tight supply and continued rental growth of prime office buildings in top global cities. In 2026, investors will be rewarded for identifying assets aligned with the future of work and living, rather than relying on a broad market rebound to rescue outdated or poorly located properties.

Late-stage & Pre-IPO companies

After several slow years, the IPO window is likely to reopen in 2026, with a strong pipeline of late-stage companies finally ready to come to market and return capital to investors. It has the potential to be a standout year, particularly for software, fintech, AI infrastructure, and defence businesses that have spent the downturn building durable revenue growth and cleaner unit economics, with names like SpaceX, Cerebras, Consensys, and MiniMed already lining up filings or targeting early 2026 listings.

Regarding tech, 2026 will likely be another blockbuster year for AI, as the industry remains the primary driver of growth. However, it may also reveal which businesses have strong fundamentals and which have been driven upward by the hype. Access to these late-stage opportunities will continue to broaden as platforms such as Wealt, which syndicate allocations into growth and pre-IPO deals, become a mainstay for private investors seeking exposure to this previously institutionalised asset class. The key for the year will be carefully sifting through and selectively backing late-stage companies most likely to thrive as public businesses, unlocking value just before they enter public markets in a way that is more accessible than ever.

.png)

The expanding role of private wealth

High-net-worth individuals (HNWIs) and family offices are becoming a visible force in private markets. With other areas of the market in turmoil, they have stepped in to fill funding gaps, often moving faster and with more flexibility than significant funds. As private markets expand beyond traditional institutions, tools such as co-investments and SPVs are giving private wealth investors greater control over how they allocate, structure, and time their participation.

Wealt is leading the change toward opening private markets that have traditionally been reserved for the top 1% and large institutional investors. Through technology and innovation, Wealt is opening doors and enabling you to access private-market deals, changing the investment landscape for many.

- Low fees - Private markets typically involve high management and performance fees, which can eat into returns. Wealt lowers both the entry barrier and overall fee load, allowing you to invest with smaller minimums and keep more of your upside.

- Transparency - Information about private investments is often less transparent than that of public markets, making it challenging for investors to assess risks and performance. Wealt offers transparent expense sheets and real-time updates about your investments.

- Liquidity - Private market investments often have long lock-up periods, limiting access to capital when needed. Wealt creates platform liquidity for secondary-market transactions among syndicated investors within Wealt Club.

With these policies, Wealt is trying to democratise processes in private markets, creating a hub for fairer investments. Join over 1400 members today, and let's democratise private market access together.

Portfolio construction for 2026

In 2026, it's essential to understand your objectives and prioritise these during portfolio design. Private markets offer investors the potential for varied long-term returns and provide diversification at a time when stock-bond correlations are higher than they used to be.

Building blocks

These are the core building blocks of a private markets portfolio in 2026. Each asset class specialises in a different role, whether that is driving long-term returns, delivering steady income, or smoothing liquidity and risk over time.

- Growth engine - The growth engine focuses on long-term capital appreciation, primarily through private equity, growth equity, and late-stage venture. In exchange for higher volatility, longer lock-ups and company-specific risk, this block seeks a return premium over listed equities and can often be the primary driver of long-term portfolio growth.

- Income engine - The income engine aims to generate contractual, recurring cash flows through private credit, core real estate and infrastructure. These strategies are designed to deliver a steady yield, whether from floating rate interest on loans or inflation-linked cash flows from essential infrastructure. Although they remain illiquid compared with listed bonds, they help preserve capital in real terms and are willing to trade some upside for greater stability.

- Diversification and liquidity engine - The diversification and liquidity engine focuses on smoothing returns and managing capital access. It typically uses secondaries, evergreen funds, and other structured solutions to mitigate the J-curve effect, accelerate distributions, and rebalance across vintages. This block can add instant diversification across managers, sectors, and geographies, while periodic liquidity windows provide greater flexibility than traditional vehicles.

Portfolio construction considerations

With 2026 shaping up to be a constructive yet still uncertain year, portfolio construction must balance optimism with caution. Investors need to carefully consider how their private markets exposure will perform across different macro, political, and market scenarios. A few core principles help guide that process before deciding how much to allocate to each building block.

- Know each building block's role - Every allocation should have a specific role in the portfolio, whether it is growth, income, inflation protection or liquidity management. Being explicit about the role of each strategy makes it easier to size positions and decide where to adjust when conditions change.

- Build portfolios patiently - Spreading commitments across multiple years and strategies, rather than concentrating the entire allocation in a single vintage, can help avoid timing risk and provide flexibility to capitalise on volatility.

- Purposefully plan liquidity - Given the long holding periods in private markets, secondaries, and other structured solutions, these should be built into the plan from the outset to provide predictable access to capital when needed, rather than relying on unpredictable sales.

- Maintain discipline in cycles - While current market conditions support a more opportunistic approach, it's critical to focus on long-term value creation through resilient structural themes rather than short-term economic cycles.

How should you approach 2026?

If 2025 was about rebuilding the foundations of private markets, 2026 is about identifying the sources of true quality. The environment now rewards businesses with real cash flow, operating leverage, and exposure to durable structural growth themes, including AI, the energy transition, critical infrastructure, and the future of living and work. For investors, it means being disciplined about which managers and assets can translate those themes into resilient earnings and distributions.

It's also important to recognise that while the backdrop is more stable than in the immediate post-pandemic years, there are still clear risks that could shape outcomes in 2026 and beyond:

- Economic slowdown or a renewed inflation that keeps rates higher for longer.

- Overconcentration in AI and a narrow set of technology names creates valuation and crowding risks if growth expectations are missed or sentiment reverses.

- Geopolitical shocks that disrupt supply chains, capital flows or energy markets.

- Liquidity mismatches in semi-liquid and evergreen structures could arise if redemptions increase as exits slow, leading to delayed payouts or discounted asset sales.

In that context, deep research, selective access and disciplined portfolio construction are key. The most robust approach is to be explicit about objectives, use private markets as growth, income, and diversification engines, and plan liquidity from the outset. Platforms like Wealt are designed to support that shift, helping investors access high-quality opportunities across late-stage tech, AI, defence and energy while lowering barriers on minimums, fees and transparency. Used thoughtfully, tools like this can help turn the themes that define the next decade into a focused, resilient private markets allocation.