Value Investing in Late-stage Startups

Explore how value investing principles apply to late-stage startups and secondaries, plus how to access them.

Investing in startups is risky. According to Shikhar Ghosh, 75% of venture-backed start-ups will likely fail. This failure rate could be intimidating without knowing its values, especially for late-stage startups. Late-stage startups are more established, which means they are closer to profitability or already profitable, have established business models which grow at a higher rate than their public counterparts, and show strong market traction. And if you are willing to go through all the risks, there is a lot of value waiting for you. The important thing is to know how to apply the principles of value investing to late-stage and pre-IPO scenarios and what the largest PE and VC firms are doing in the secondary space. Most importantly, you don’t need to be a fancy institutional investor to run these strategies; with the network and opportunities brought to you by Wealt Club, all you need to do is download our app and join the community of sophisticated investors.

What is value investing?

Value investing is an investment strategy in which investors purchase assets or stocks, believing the market price is below their estimated intrinsic value. The concept is simple: if you know the true value of an item, you can save lots of money by determining the time of your shop. The same goes for the investment. As an investor, you can purchase value stocks at lower prices and have an opportunity to sell at the high when the prices correct themselves. According to the Security Analysis book by Benjamin Graham and David Dodd, the holy book of Value Investing, Graham says investors should focus on purchasing securities at prices less than their “true” value.

Value investing principles and Warren Buffett's strategy

From value investing principles and one of the best-known value investors, Warren Buffett, we have gathered several key principles to guide you through your value investing.

Margin of safety

The margin of safety principle is a concept that suggests that you should only purchase a security at a price that is wide differential from the intrinsic value of the security in question. This helps minimise the potential for sizable losses due to flawed analysis or other market anomalies. For example, suppose the company’s intrinsic worth has been appraised at $ 100 per share. In that case, a value investor may wish to pay anything between $ 70 and below to safeguard against any possible mispricing or bad downturns in the market. 30% or higher discount is widely used as a common denominator in value investing, partly because historical 1-year annual volatility of the stock market is seen in worst years.

Quality over quantity

Buffet advocates investing in companies with strong fundamentals, such as sound earnings and good cash flows, that dominate their relevant sectors. Accomplished investments are more capable of withstanding the adversities of economic depressions and consequently produce steady eventual returns. For instance, an investment in a highly branded firm with loyal customers and regular earnings would be of great quality in the market, contrary to an investment in a volatile firm with unpredictable earnings.

Concentration over-diversification

Although it is not wrong to diversify your portfolio and not risk all your money on a single investment, Buffet disagrees with excessive diversification and goes for well-researched conviction investments. He prefers a concentrated portfolio of 10-12 companies. This is because it enables investors to dedicate more capital to their strong probable positive outcomes, which may increase returns. Unlike many VCs, who bet on the spray-and-pray approach of 20-30 companies in a fund, outliers with higher returns have used a more concentrated approach and their industry-specific expertise to capture returns.

How value investing can apply to growth late-stage startups

Late-stage startups have already raised significant funding, proven their business model, achieved market traction, and started their profitability era. While these startups bring significant value investment opportunities, applying the concept of value investing to these startup businesses allows the investor to see value in these businesses whose stocks are undervalued yet endowed with tremendous growth prospects.

Late-stage and pre-IPO companies sold at deep discounts compared to public competitors

Late-stage startups and pre-IPO companies tend to have a lower valuation than publicly listed companies. These differences are observed due to various factors, such as private equity investments being relatively less liquid, being perceived at a higher risk than public investments, and the pool of investors being limited compared to the public markets. However, for value investors, these cuts are a positive signal for a chance to buy a piece and turn it into an attractive and promising business for bargain prices. For instance, a tech startup at the final stage, generating high revenues, might be priced 30% cheaper compared to its peers in the stock market, which has a very good potential if the company moves to the next stage, producing and listing shares for investors.

Pre-IPO buying companies offer higher growth than their public counterparties.

Investing in late-stage startups allows the investor to access a firm on the verge of hitting its major growth performance indicators like listing on the stock exchange. Such businesses tend to experience higher revenues per growth rate and be more innovative than the typical public firms, with higher returns on investors’ stakes.

The level of risk for investing in late-stage startups is mitigated as they move to profitability.

The risk factor remarkably reduces over the lifecycle of a startup; with increased growth and the movement towards profitability, their fundraising capacity increases and their potential IPO can be in the foreseeable future. After series C, a startup’s chance of failing is 1%, while the chance is 60% until series A. Late-stage startups can show sustainable growth with high revenues and sound economic viability as they move up in the ranks of scaling their business. What value investors can take advantage of is that they can focus on investing in companies that show resiliency, strong cash flow growth and a sticky customer base, while less than 5% of startups break even on their cash flows. For example, a late-stage company making reasonable profits, especially if it has a distinct realistic plan for expanding its operations, will likely offer a comparatively lower risk proposition than the early-stage companies still exploring their markets.

Is buying global top 50 startups better than buying ETFs?

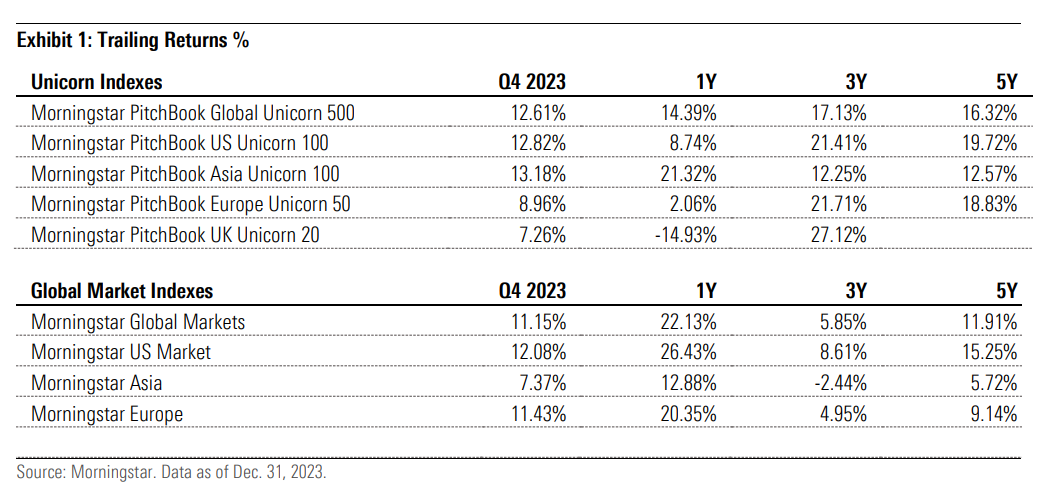

Investing in 50 global startups may generate more returns than ETFs indexing standard equity markets. The Morningstar Unicorn Market Monitor: Q4 2023 shows a 16.32% 5-year return for global unicorn indexes, outperforming global markets' 11.91% 5-year return. Such top startups are typically market leaders or contenders against market leaders in their sub-industry. They are ideally situated to extend their growth rates and capture a big stake in the market share. The US Unicorn 100 and Europe Unicorn 50 indices stand out with 19.72% and 18.83% 5-year returns, respectively, significantly surpassing their corresponding regional market indices. Nevertheless, this strategy entails stringent analysis and possession of pertinent information concerning each company's different risks and opportunities.

What the biggest PE/VC funds are doing in secondaries?

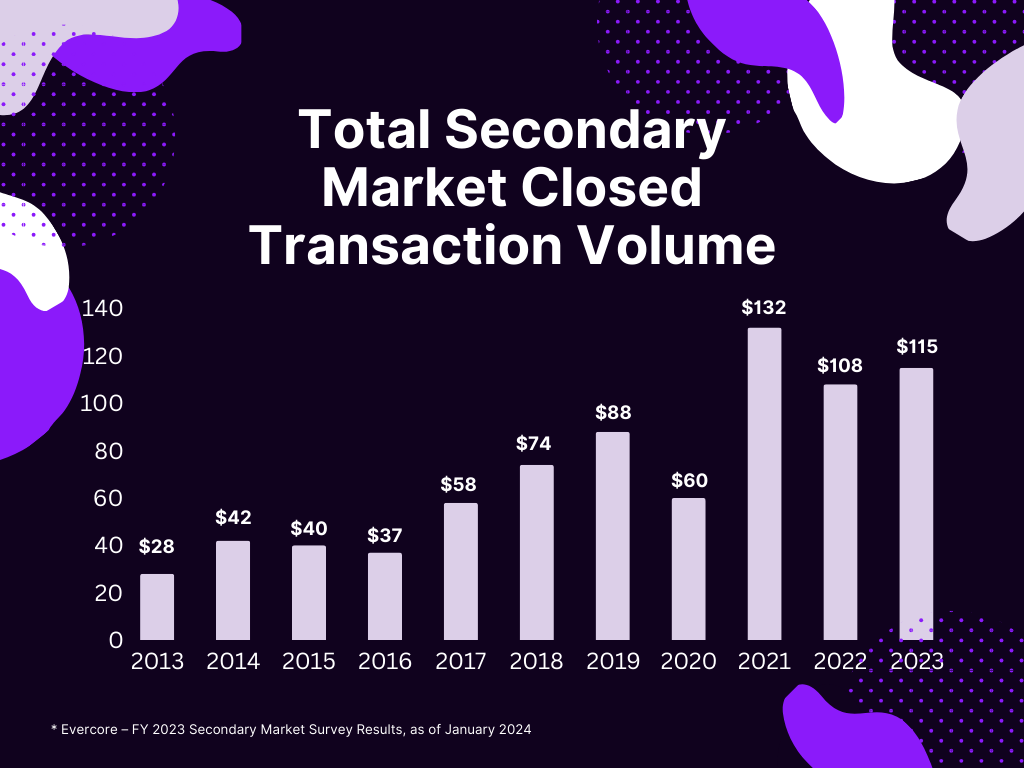

In recent years, we have seen significant growth in the secondary market for private equity and venture capital investments, with 4x market growth in 10 years in the total secondary market closed transaction volume. Also, secondary fundraising hit a record $93.8bn in 2023 and still has plenty of room to grow.

Big PE/VC funds are raising huge amounts of money to buy back secondaries.

Major PE and VC funds leverage significant funds to buy secondaries through late-stage startups. The target market remains attractive since these funds understand the opportunity the secondary market represents in acquiring high-growth companies at bargain prices. Here are some notable examples of big secondary funds:

- Blackstone closed its secondary private equity fund at $22.2 billion and became the world’s largest secondary fund, while its previous fund closed at over $11 billion in 2019.

- Ardian has raised over $20 billion to buy stakes in private equity funds from investors and aims to raise $25 billion for the next fund.

- Lexington Partners closed at $14 billion for its latest secondary while closing at $10.1 billion in 2015.

- Partners Group launched a $12 billion private equity secondary fund, while roughly 20% of the nearly $150 billion Partners Group managers in private markets have been deployed to secondary transactions.

These funds are usually dedicated to secondary market investments and seek to purchase high-quality assets at reasonable prices. Eventually, they give their investors great chances of earning high profits while avoiding excessive risks.

These large funds are raising capital and actively participating in secondary transactions to manage secondary portfolios and provide liquidity solutions. The rise of the secondary fundraising rate signifies the emerging market's strategic importance. By 2030, it could evolve into one of the primary investment strategies for all mature private market portfolio investments, accounting for between $200 billion and $500 billion.

How can individual investors deploy similar strategies?

Individual investors can replicate what large funds in PE and VC firms are doing by participating in the secondary and primary rounds of matured late-stage startups. Going further down the line, they can invest alongside major PE/VC firms to capture potential growth and diversification with a concentrated approach with like-minded value investors deploying in their strategies. With a clear margin of error, around 30% offers an upside of %50; given the high single-digit return you can extract from the public market over the long term, the compounding effect of a discounted quality asset portfolio can easily offer 10x more wealth growth in 20 years.

Build your portfolio via Wealt Club.

One platform is Wealt Club, which enables individual investors to apply value investing in late-stage startups such as SpaceX, Anthropic, xAI, Klarna, Groq, and many more. Through Wealt Club, investors get access to a handpicked selection of the late-stage startup ecosystem and secondary and primary round opportunities at lower minimums (from $5,000), thus benefiting from the same forces that make successful PE and VC investments work.

Wealt Club provides detailed information and analysis on each investment opportunity, helping investors make informed decisions. Additionally, the application offers a way to manage and monitor investments, ensuring investors can effectively implement value investing strategies and achieve their financial goals.